Executive Summary

The global economy demonstrated resilience in 2024, avoiding a widespread contraction despite consecutive shocks and sustained inflation-driven monetary tightening. Near-term global growth is expected to remain stable but subdued. While disinflation and monetary easing in many countries may boost demand, ongoing conflicts, and geopolitical tensions could worsen supply-side challenges. Additionally, tight fiscal conditions and lingering debt issues in developing nations will constrain investments and growth.

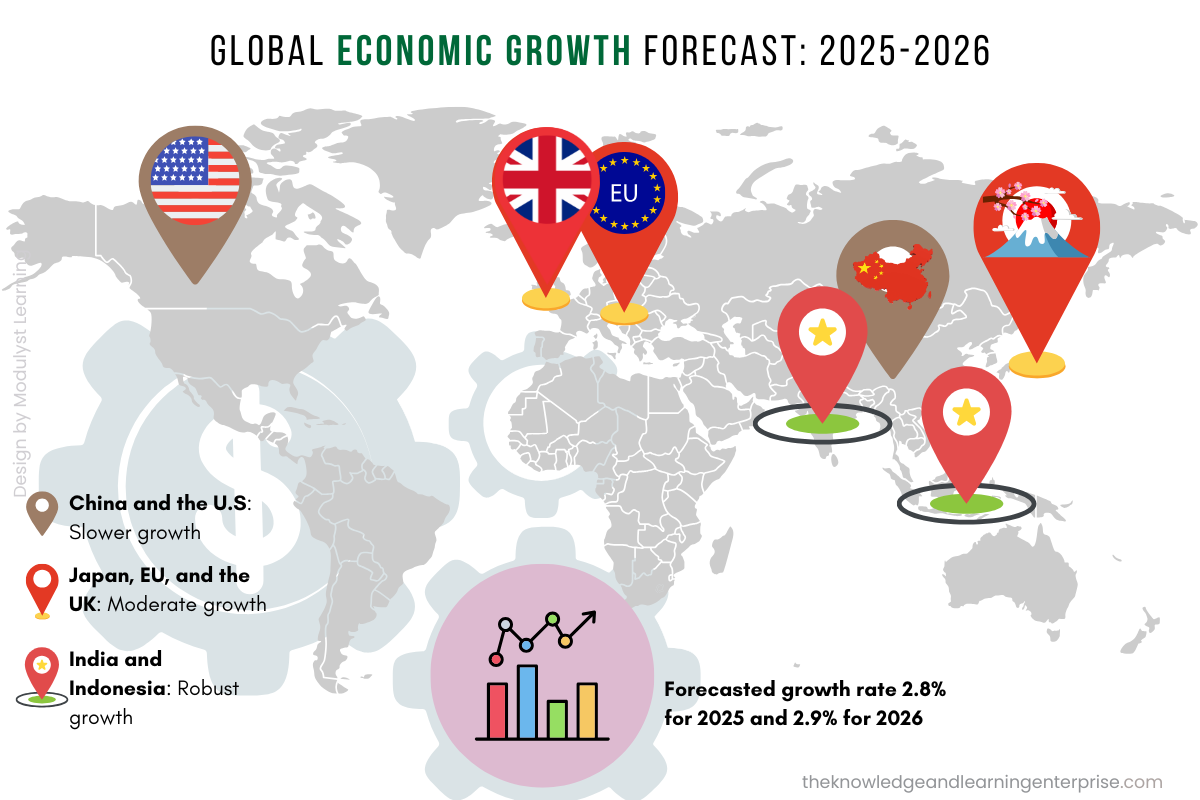

Growth Forecasts

Global economic growth is forecast at 2.8% for 2025 and 2.9% for 2026, similar to the 2.8% recorded in 2023 and projected for 2024. Slower growth in China and the U.S. will pair with modest recoveries in the EU, Japan, and the U.K., while India and Indonesia are expected to perform robustly. However, the short-term outlook for low-income and vulnerable countries remains less favorable, with revised-down growth projections for least developed countries (LDCs) despite a slight improvement in 2025.

Global growth remains below the 2010–2019 pre-pandemic average of 3.2%, reflecting structural challenges like weak investment, slow productivity, high debt, and demographic pressures. Many developing nations still struggle with the pandemic’s long-term effects and recent economic shocks. While the green transition and technological innovation could spur growth, these benefits are likely to concentrate in developed economies. Developing nations face hurdles in financing infrastructure, technology, and human capital investments, limiting their ability to ascend global value chains.

Although downside risks to growth have lessened since 2023, uncertainties persist. Positive trends in 2024, such as widespread disinflation and monetary easing by major central banks, improved the global financial environment. However, geopolitical and economic uncertainties remain elevated, as highlighted by the Global Economic Policy Uncertainty and geopolitical risk indices.

While global inflation has eased, disinflation has slowed, driven by persistent housing and service sector price pressures in developed economies. If inflation resurges, central banks may slow rate cuts, keeping policy rates higher than pre-pandemic levels. High borrowing costs and debt challenges will likely persist, heightening the vulnerability of developing economies, many of which face severe debt distress.

Download the full article to read it offline:

{kind=link}

Want to stay informed and inspired? Subscribe to our blog for insightful updates delivered straight to your inbox. Explore our website for a curated collection of reference books, resources, and more – designed to fuel your curiosity and keep you ahead.